Summary

- After plunging sharply in the third quarter, loans are expected to slightly improve on the back of decent economic activity in operating region.

- Non-interest expense is expected to drag earnings next year.

- Quarterly dividend is expected to be maintained at $0.14 per share in 2020, implying a high dividend yield of 4.32%.

- The current stock price is very close to the estimated one-year ahead target price. Therefore, BCBP is not a good buy at current level.

BCB Bancorp's (NASDAQ:BCBP) third quarter results were mostly in line with expectations. However, the significant 2.0% quarter-over-quarter decline in loans gave a negative surprise. Going forward, loan growth is expected to slightly recover, but it will most likely not be sufficient to counter normal growth in non-interest expense. Consequently, I'm expecting earnings to decline in 2020 compared to 2019. Despite the earnings decline, I'm expecting next year's dividends to be maintained at current level.

Loan Growth Likely to Recover

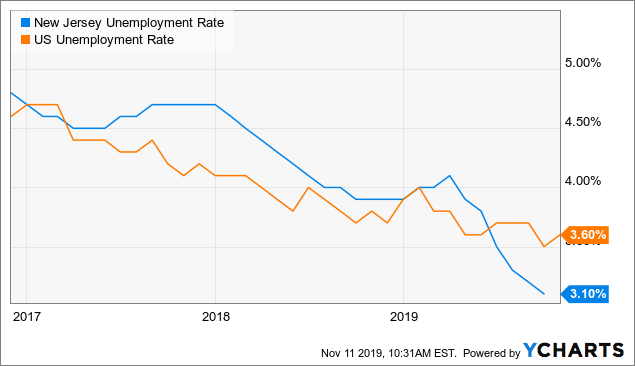

As mentioned in the 3QFY19 earnings release, loans decreased in the third quarter compared to the second quarter of 2019 as the management focused on re-positioning the balance sheet, which included curtailing loan growth and strengthening the capital position. Going forward, loan growth is expected to somewhat improve due to decent economic activity in the company's main operating region. BCBP focuses on residential and multi-family mortgages in New Jersey, which is why the strength of the housing market and unemployment are two important drivers for demand of the company's credit products. New Jersey's unemployment has improved remarkably in recent times, as shown in the chart below. The low unemployment will encourage greater demand for mortgage loans in the coming quarters.

Data by YCharts

Data by YChartsThe company also operates in New York, where the rent control regulations can limit growth. However, the concentration in New York is not at a problematic level as BCBP has 3 branches in the state, as opposed to 30 branches in New Jersey.

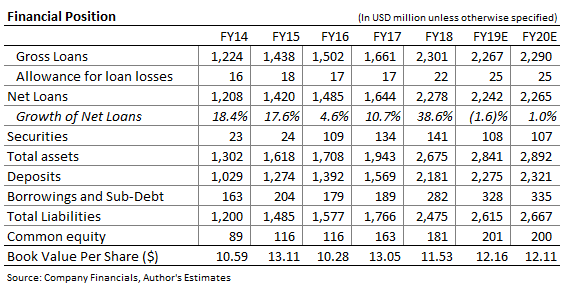

Based on the above-mentioned factors, I'm expecting BCBP's loan growth to improve slightly in 2020 to 1.0%, as shown in the table below.

Re-pricing Gap to Benefit Margin in the Near Term

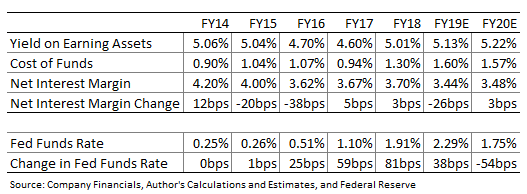

BCBP's assets consist primarily of mortgage loans; therefore, the assets carry longer maturities than liabilities, which mainly consist of deposits. Due to this re-pricing gap, BCBP's net interest margin, NIM, is expected to rise slightly in the near term as yields will be maintained while funding cost will decline following the 75bps Fed rate cut. Towards the second half of 2020, however, it is likely that NIM will start declining as loans re-price.

Based on the re-pricing gap and my assumption of stable Fed funds rate going forward, I'm expecting average NIM in 2020 to be 3bps higher than the 2019 average. The table below shows my estimates for yield, cost, and margin.

Despite the expectation of a slight increase in both average NIM and year-end earning asset balances for 2020, BCBP's net interest income is estimated to decline next year because average balances of assets and liabilities during the year will be different from year-end balances.