Summary

- I expect earnings to decline slightly in 2020 due to lower net interest margin and higher non-interest expense.

- Loan growth rate is expected to slightly dip as the commercial real estate segment slows in the wake of the larger economic slowdown.

- I expect United Bankshares to maintain its dividends, as they appear to be at a safe level.

- The company appears to be undervalued in the market, as my target price implies a 14% upside.

I expect earnings growth of United Bankshares (UBSI), a regional bank holding company, to decline in the coming quarters, mostly on the back of lower net interest margin and higher non-interest expense. On the other hand, I expect continued loan growth to help keep earnings afloat.

Loan Growth to Buoy Earnings

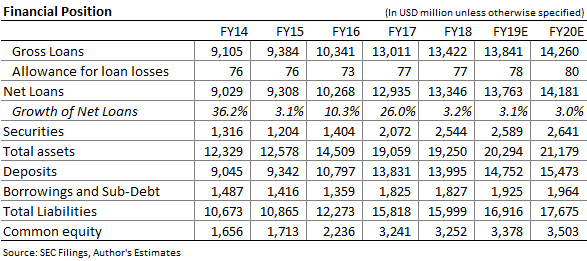

I expect loans to continue to grow at a low rate for the remainder of 2019 and in 2020. I expect loan growth to remain low, as my outlook on business activity is less than rosy in the wake of trade uncertainty. UBSI operates in the Washington, DC, and Virginia areas, with commercial real estate being its biggest focus class; hence, I believe that business sentiment is an important driver for the company's loan growth. The table below shows my estimate for UBSI's loans and other balance sheet items.

In the latest investor presentation, management noted that they expect loans and deposit growth rates to be in the low- to mid-single digit range for 2019.

I expect expansion in the loan portfolio to require greater reserves and, consequently, higher provisions charge for credit losses in the quarters ahead. My forecast for provisions charge is shown in the table further below titled "Financial Summary". As the provisions charge has been very low in 2019, the expected growth does not appear material.

Net Interest Margin to Constrain Earnings Growth

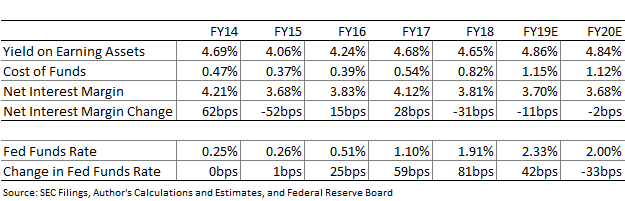

One of the major contributors to my expectation of slight earnings decline is net interest margin. I expect net interest margin to decrease in the coming quarters due to the Fed Funds rate cut that will put yields under pressure. While funding cost will also be affected by the Fed Funds rate cut, that effect is unlikely to completely counter the impact of lower yields. Further, I expect little relief from deposit mix, as the proportion of non-interest bearing deposits in total deposits declined to 30.1% by the end of June 2019, from 31.6% at the end of December 2018.

I expect both yields and costs to dip by 4bps each in 3QFY19 and 4QFY19. For FY20 I expect yields to decline by 2bps in the first quarter and another 2bps in the second quarter as a result of a lagged effect of the 50bps rate cut in 2019. I am not expecting any further monetary easing in the country. The expected combined effect will be a reduction in net interest margin of 11bps in 2019 and 2bps in 2020. The table below summarizes my yields, costs, and margins expectations.

In the latest investor presentation, management's guidance indicated expectation of slight decline in net interest margin.