Summary

- We expect the upcoming acquisition of 8 branches to lead to strong growth in earnings assets, which will help boost BHB's bottom-line.

- Earnings are expected to also receive support from BHB's focus on low cost deposits and wealth management services.

- Our target price suggests only a 5.6% potential upside to BHB's market price.

Earnings of Bar Harbor Bankshares (BHB) have declined in the first half of 2019, but we expect them to improve on the back of the company's acquisition of eight bank branches. We expect the company's bottom-line to also receive support from net interest margin and non-interest income.

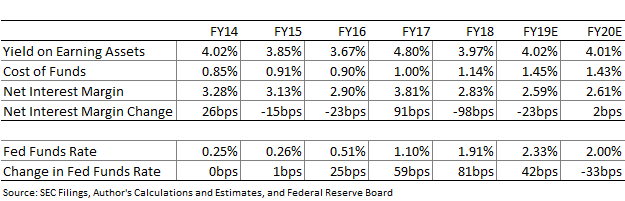

Lower Funding Cost to Support Margin

We expect cost of funds to decline in the future due to the 50bps Fed Funds rate cut in 2019. Furthermore, funding cost will also be positively affected by the company's increased focus on building non-interest bearing deposits, which increased by 12% year-over-year in the first six months of FY19. However, BHB's average non-interest bearing deposits declined in 2QFY19 compared with 1QFY19.

We expects yields to also decline in the remainder of the year due to Fed Funds rate cut, which will affect floating rate loans this year. We do not expect BHB to cut its yields sharply for new loans as the company noted in its latest 10-Q filing that it is concentrating on opportunities with proven borrowers regardless of competitive pressures.

The table below shows our projections for BHB's yields, costs and margins. Please note that the margin is showing a decline in 2019 due to the decrease in the first half of the year.

Acquisition of Maine Branches to Support Growth of Earning Assets

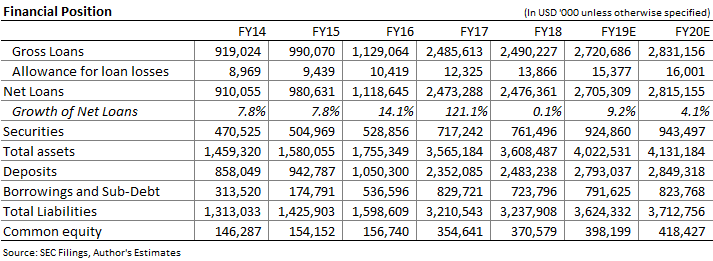

As noted in the latest 10-Q filing, BHB's management hopes to complete the acquisition of eight branches in central Maine in 4QFY19. These branches have $287 million worth of deposits and $111 million loans. Consequently, we expect BHB's net loans to rise by 5.0% in 4QFY19, taking the full year growth to 9.2%. Apart from the acquisition, there is little reason for loan growth due to our outlook of economic slowdown. BHB's biggest segment for loans is residential real estate, and the housing market has been showing signs of slowdown since early 2019. Housing starts did rise to a 12-year high in August, but we expect it to have been an anomaly. The table below shows our projections for BHB's key balance sheet items.

Non-Interest Income to Further Support Earnings

Non-interest income was one of the main drivers of income in 2QFY19. Going forward we expect non-interest based income to further grow as the company plans to start focusing on wealth management business. In 2QFY19 BHB hired a President of Wealth Management who will lead the business as one collective organization. We expect non-interest income to grow 10% in 4QFY19 and then 14.5% in FY20.

Due to support from loan growth, net interest margin and non-interest income, we expect BHB's earnings to grow by 21.7% in FY20. The table below shows our earnings estimates.