Summary

- BCBP's balance sheet and income have surged in 2018 and 1H2019 due to a merger. Going forward, growth will normalize.

- We expect NIM to face some downward pressure in the remainder of 2019 due to the Fed rate cut. NIM is likely to stabilize in 2020.

- Our valuation analysis shows that the stock is slightly overvalued, hence we recommend buying only on dips.

Following the acquisition of IA Bancorp last year, BCB Bancorp (BCBP) appears to be on a growth trajectory. Earnings of the community bank holding company are already up 53.7% in the first half of the year. As the growth spurt was attributable to the merger, we expect growth rate to decline and earnings to stabilize for the remainder of the year. For FY20, we expect earnings to increase by 3.8% on the back of an increase in net loans. We also expect the company to maintain its dividend at the current level, which implies a 4.32% dividend yield.

Loan Growth Rate to Decline

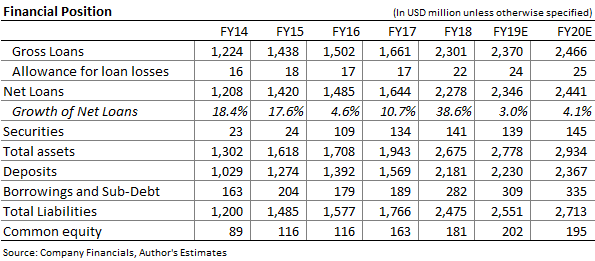

Loan growth had been unusually high in 2018 due to BCBP's acquisition of IA Bancorp. As no announcements regarding future mergers have been made, we expect loan growth rate to return to a lower level in the remainder of 2019 and 2020. Prospects of economic slowdown in the country will also restrain appetite for credit, especially in the commercial segment. The table below shows our estimates for BCBP's net loans and their growth rate.

NIM to Decline in the Remainder of 2019

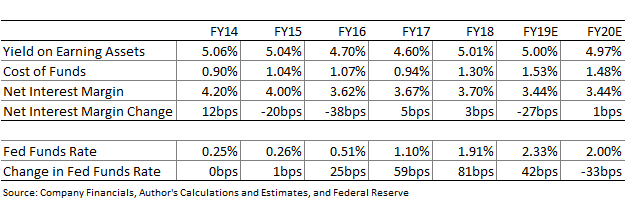

We expect BCBP's net interest margin, NIM, to decline in the remainder of 2019 as the 50bps cut in Fed Funds rate will lead to a dip in the company's yields on earning assets. The effect will be somewhat countered by a lowering of rates on deposits. A favorable deposit mix will also help cancel out some of the effect of lower yields. BCBP's deposit mix has shifted towards non-interest bearing deposits in 2QFY19, which we believe will help keep costs low in the rest of the year and in 2020. Non-interest bearing deposits rose to 12.6% of total deposits at the end of June 2019, from 12.1% at the end of December 2018. We are assuming that BCBP will be able to maintain this deposit mix in the near future, which will keep the cost of funds low in the coming quarters.

Overall, we expect average NIM in 2019 to be 26bps below NIM in 2018. For 2020 we expect NIM to be mostly unchanged as we are not expecting further interest rate cut. The table below shows our projections for yields, cost of funds and NIM of the company.

Admin Expenses to Return to Normal Growth

BCBP's non-interest expenses were almost unchanged in first half of 2019 from the corresponding period of 2018 as the absence of merger related expenses made up for greater salary expense and other administrative expenses. Going forward we expect BCBP's administrative expenses to rise at a natural rate of 1% quarter over quarter.

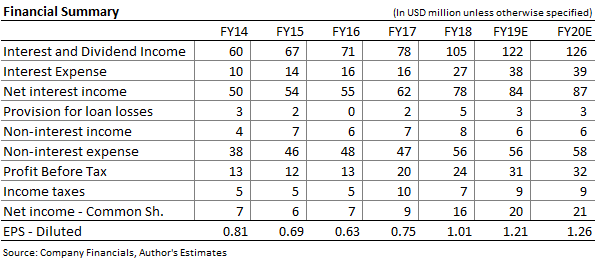

Mostly due to the loan growth, we expect BCBP's earnings to grow by 27% to $1.21 per share in 2019. The table below shows our earnings estimates for the company.

Dividends to be Maintained

BCBP has consistently given a quarterly dividend of $0.14/share since 2Q2014. The estimated payout ratio is at a comfortable level of 47.9% for 2020 (assuming the dividend is maintained) and the bank's Tier I ratio of 11.57% is above the regulatory requirement of 6.00%. Therefore, we foresee no trigger that could force the company to break its tradition of paying $0.14 per quarter.

Our dividend forecast implies a forward dividend yield of 4.32%.