Summary

- The Hershey Company has seen shares rapidly appreciate in a matter of months, after a strong Q1 report ended what has been years of range-bound trading.

- Hershey currently isn't poised to realize explosive revenue growth, but shifting consumer trends, potential pricing increases, and international growth should place growth at a solid floor.

- We like shares if a market pullback affords us them in the $125 range.

Stocks of high-quality companies typically command premiums in the market. They are usually a bedrock of stability when the economy/market turns lower. On the other hand, they can become bloated when things get too hot. This appears to be the case with The Hershey Company (HSY). The leading (public) confectionary company in the United States, Hershey is a business that prospers through all economic environments because chocolate is essentially recession proof. Hershey's stock has traded range bound between $90 and $110 for much of the past five years before busting out at the beginning of 2019. Now near highs at $146, the stock has gotten a little ahead of itself. Even high-quality companies can make for poor investments if the valuation is too high. We will identify where we feel shares need to fall to, and some growth drivers that could benefit the company over the long term.

Source: YCharts

Source: YCharts

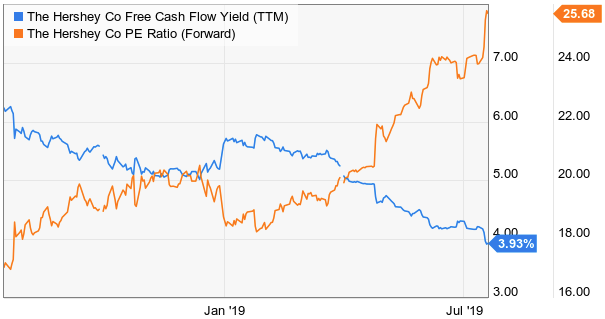

The appreciation of Hershey's stock has been extraordinary over the past six months. We were bullish on the company a few months ago despite the stock trading at 52-week highs at the time. Since then, Hershey's strong 2019 first-quarter report and upward market momentum has carried the stock to new highs. With management affirming its FY2019 guidance last quarter, the approximate midpoint of $5.70 per share puts the stock at 25.61X full year earnings. While this seems steep, it's actually in line with the stock's 10-year median PE ratio (which goes to show the premium that Hershey commands considering just mid-single-digit revenue growth).

Source: YCharts

Source: YCharts

At the same time, the stock's 36% run in just the past six months likely means that we are closer to a near term "top" than not. After years of range-bound trading, Hershey has now become a little too rich for us. With modest growth projected over the long term (management is projecting 2-4% revenues growth and 6-8% EPS growth as "long-term" targets), it's important to avoid wandering into upper 20 something PE ratios. If everything stays the same, we like shares up to 22X earnings, or $125 per share.

There are some potential tailwinds on the horizon however. There are rumorsthat privately owned arch rival Mars (maker of Snickers and M&Ms) is increasing its wholesale prices 9%. Considering that Mars and Hershey combine for a majority of the confectionary market share in the US, such a price increase would leave room for Hershey to follow suite in some manner.