Summary

- Legg Mason's asset management business remains under pressure.

- LM has managed to stabilize asset flows, but margins are still a concern.

- Given industry challenges, the stock looks cheap for good reason.

There is no doubt about it; Legg Mason's (NYSE:LM) stock is cheap. The company trades at a forward P/E of 10 or 13 (depending on your data source). However, as an asset management company, its business is currently facing significant disruption. EPS is projected to be essentially flat over the next five years, but investors may be right to wonder if even this projection will end up being optimistic.

Legg Mason and the Asset Management Business

We think that the most important factor that will determine whether or not LM is a good investment over the coming years is what happens in the asset management and mutual fund industry itself. Assets are flowing out of high fee equity mutual funds and into lower fee index funds. You can already see the effects on LM's financial results. Revenue and operating income have almost been stagnant with revenue up 1.15% annually over the past five years and operating income up 1.7% annually over the past five years.

This performance may seem a bit surprising at first. Company AUM has actually increased over the past three years.

| In $B | 2017 | 2018 | 2019 |

| AUM | $758.0 | $754.1 | $728.4 |

| % YoY | .5% | 3.5% | |

| Net client flows | -$8 | -$22.6 | -$28.9 |

(Source: Company financials)

However, we can see that the AUM gains can mostly be chalked up to rising equity and bond markets. Net client flows have been negative for each of the previous three fiscal years. One bright spot, net outflows have been moderating and improved from $28.9B in outflows to "just" $8B last fiscal year.

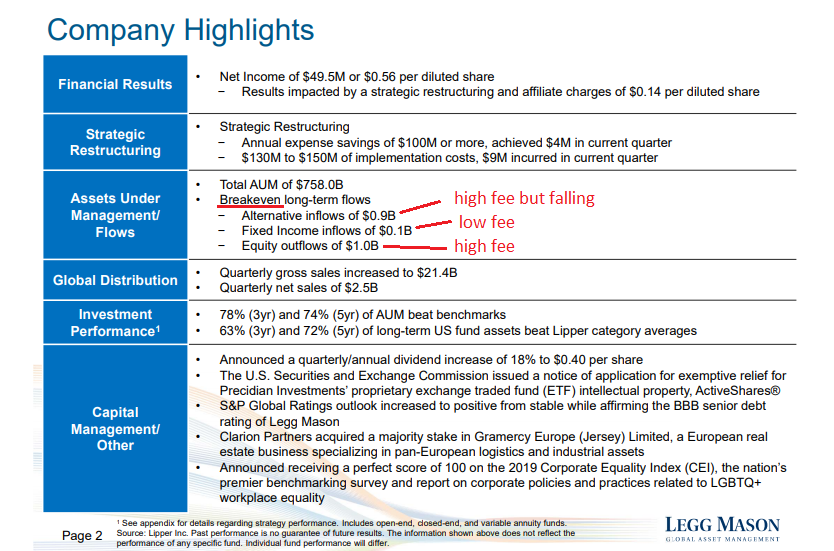

While the company touts breakeven (or even lately, growing) AUM, it's important to keep in mind what is happening "under the hood".

(Source: Investor presentation; highlights author)

Assets are flowing out of the high-fee, high-profit-margin equity segment. The assets that are growing and seeing inflows are the lower-fee fixed-income assets and alternative assets. While alternative assets have fees that match or exceed equities, they are experiencing fee compression as well.