Summary

- PepsiCo. released its second-quarter earnings for 2019 on Tuesday. The company was able to beat on EPS, and revenues were in line.

- The company is seeing growth across all of its business segments.

- Despite a solid quarter, we view PepsiCo as a hold at this time due to the valuation of shares.

Beverage and snack giant Pepsi Co. (PEP) released its earnings for the second quarter of FY 2019 on Tuesday. The company turned in a solid performance with in line revenues and a modest beat on EPS. We will look at some of the noteworthy developments from the quarter, as well as revisit the stock's current valuation. At the end of the day, Pepsi remains a strong investment option for long-term investors, but we fail to identify a buying opportunity at this time.

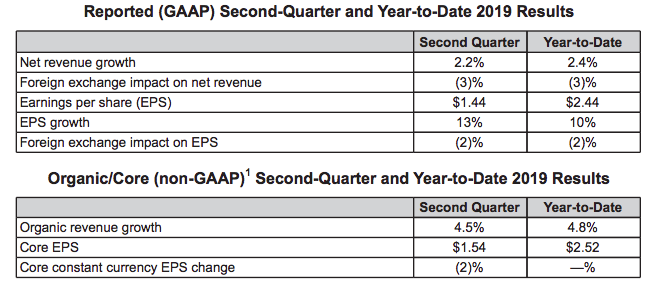

PepsiCo turned in a solid performance for Q2 2019. The company's sales were in line with consensus estimates at $16.45 billion (+2.2% Y/Y). Earnings per share were a modest beat at $1.54 on a non-GAAP basis (beat of $0.03 per share). On a constant-currency basis, revenue growth was 4.5% for the quarter and 4.8% YTD. For a mature company such as PepsiCo, we like to see mid-single-digit top-line growth.

PepsiCo turned in a solid performance for Q2 2019. The company's sales were in line with consensus estimates at $16.45 billion (+2.2% Y/Y). Earnings per share were a modest beat at $1.54 on a non-GAAP basis (beat of $0.03 per share). On a constant-currency basis, revenue growth was 4.5% for the quarter and 4.8% YTD. For a mature company such as PepsiCo, we like to see mid-single-digit top-line growth.

Source: PepsiCo, Inc. Q2 8-K

Source: PepsiCo, Inc. Q2 8-K

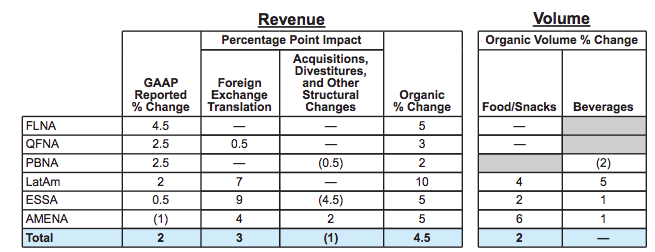

When we take a closer look at revenue growth, we see that growth was present across all segments of PepsiCo. The food and snack brands continue to drive growth for PepsiCo as a whole. Frito-Lay North America was up 5% on pricing, while Quaker North America was up 3% - its largest growth number in three years. In emerging markets, it was volume-driven gains that helped push revenue higher. Overall revenue growth was comprised of 2% volume gains and 2.5% pricing.

Source: PepsiCo, Inc. Q2 8-K

Source: PepsiCo, Inc. Q2 8-K

The company is investing into emerging brands to make sure that revenue growth continues in the years ahead. Marketing expenses increased 56 basis points (as a percentage of sales), and management is putting money into data analytics, capacity, and more. Furthermore, the company is continuing to develop growth brands such as Gatorade Propel, LIFEWTR, Gatorade Zero, and bubly - which management is optimistic about becoming a billion-dollar brand.

The last items of note from the quarter touch on some financial aspects of PepsiCo. The company continues to spend capital, with FY2019 totals estimated at $4.5 billion. The company's plans to return $8 billion to shareholders in the form of buybacks ($3 billion) and dividends ($5 billion) mean that management will need to tap the balance sheet to fund this since free cash flow will come in around $5 billion.