Summary

- While most industrial REITs are enjoying extraordinary price appreciation year to date, Monmouth Real Estate has underperformed.

- I will be focusing on the cash flow generators driving Monmouth with an emphasis on dividend growth.

- The potential impact of Amazon’s venture into shipping is much less severe than the media depicts and that’s precisely how I feel about Monmouth’s overhang.

- This idea was discussed in more depth with members of my private investing community, iREIT on Alpha. Get started today »

In a recent article I stated that I’m “a disciple of fundamental analysis in which I spend countless hours analyzing the sustainable competitive advantages, valuation, and margin of safety of publicly-traded REITs.”

I added that “in order to understand the true profit potential for a REIT, it’s imperative to build a model demonstrating how the company can earn their cost of capital to drive scale.”

As a REIT analyst, I’m always “surveying the list of filtered opportunities” in order to “determine the companies that generate the most reliable profits over time.” Part of the hard work not only involves the cost of capital but also the company’s free cash flow (after dividends).

In that same article I provided a list of 23 equity REITs with the overall lowest payout ratios and the sole industrial REIT on that list is First Industrial (FR), with the 10th lowest payout ratio (based on FFO) of 54.7%.

Cash flow is critical for any business and today I wanted to spend time on another industrial REIT that’s on our strong buy list. While most industrial REITs are enjoying extraordinary price appreciation year-to-date, Monmouth Real Estate (MNR) has underperformed.

As a result of this underperformance (of Monmouth) we thought it would be helpful to take a closer look at the company to determine what’s causing the lackluster performance.

Keep in mind, we upgraded Monmouth to a strong buy back in August 2018 based primarily on the robust earnings growth forecast (low double-digit) and potential dividend increases. In an article I explained that “Monmouth is in the e-commerce sector and that's precisely what's fueling the strong performance.”

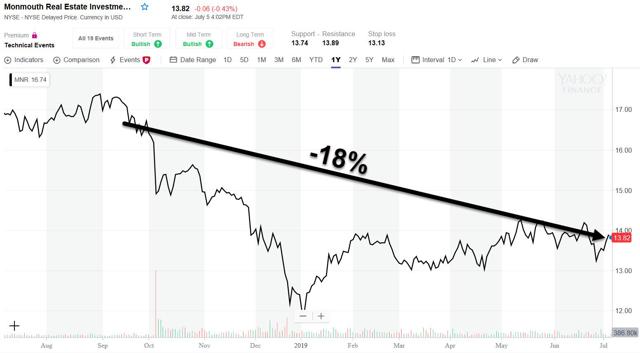

Source: Yahoo Finance

Since that time (August 2018) Monmouth shares are down another 18% and the dividend yield is now 5.02%. Compared with the closest peers, Monmouth has become an attractive strong buy, perhaps stronger than I wrote about (back in August 2018).