Summary

- Management failed to deliver in terms of cash conversion cycle so far and slashed SKU rationalization guidance.

- Proceeds from divestitures will be lower than expected and thus impact the company valuation.

- Sales and margins will be weaker than announced.

- Share repurchase-related communication has been ambiguous.

- While I remain long the stock, the investment will likely turn out less profitable than anticipated.

Overview

In my article published in late October 2018, I laid out my investment thesis for Newell Brands (NWL). I arrived at the conclusion that the company is undervalued at $16 per share and communicated conservative and optimistic price targets of $22 and $39, respectively, based on adjusted-present-value (APV) estimates. Since the share price dropped significantly in response to the FY2018 earnings call, a discussion of what has been communicated and the impact on valuation is warranted.

The SKU rationalization guidance has been cut

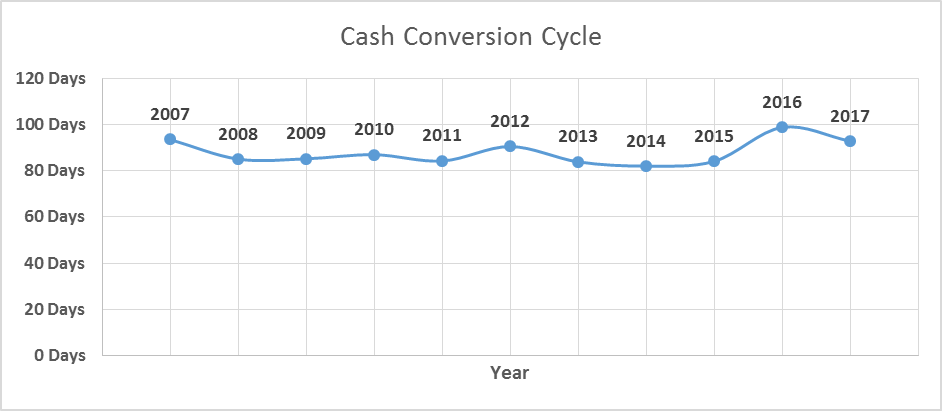

The presentation from 05/04/18, detailing the accelerated transformation plan (ATP), is still available here. Therein, management claimed that they would reduce SKU count by 51%, benefitting working capital management and thus cash flow generation capabilities. This is important since NWL’s cash conversion cycle worsened in the course of the Jarden acquisition in 2016 as can be noticed from the graph below:

Data Source: Newell Brands’ 10-K filings (2007-2017), Illustration: Author’s own work in Microsoft Excel

Data Source: Newell Brands’ 10-K filings (2007-2017), Illustration: Author’s own work in Microsoft Excel