Summary

- CHD delivered stellar results year after year both on a standalone basis and relative basis.

- The firm has a portfolio of strong brands in consumer packaged goods segment.

- Regression analysis indicates a 4.55% growth for the coming year.

- New extensions in the laundry, oral care, and personal care segments will help boost both top and bottom line.

Investment Thesis

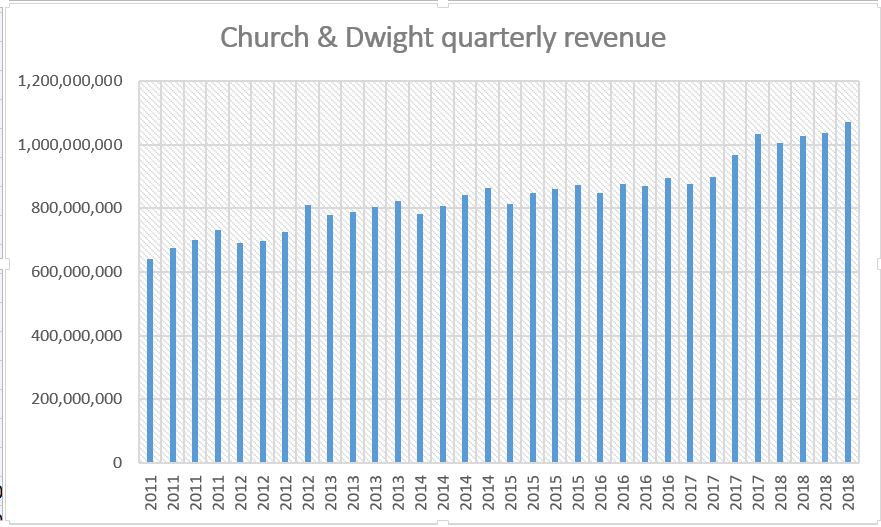

Church & Dwight (CHD) is a renowned name in the household, personal care, and specialty product markets. After studying a number of its peers, I have found that the firm has been growing at an above-average rate since 2011 along with higher profitability. The firm has 11 power brands which account for roughly 80% of its revenue. CHD features a very balanced portfolio between household and personal care market (household 45%, personal care 48%, and specialty products 7%) and also balances nicely between premium and value products (65% premium, 35% value). For the coming year, the firm expects its EPS to increase by 7% to 9% driven by operating income growth, which I think is economically achievable. Compared to the peer group average, the firm also has higher operating cash flow to revenue. The firm has a number of strong brands and has consistently delivered stellar results. Combining all the factors, Church & Dwight is a hold.

Source: Intrinio