Summary

- JNJ easily beat reduced Q3 earnings estimates.

- The healthcare company guided up for 2020, but the new estimates are still down $1 from original targets.

- The stock continues to underperform the market due to an expensive multiple from the dividend aristocrat status.

- Investors should only buy JNJ on dips.

- Looking for more investing ideas like this one? Get them exclusively at Out Fox The Street. Get started today »

For years now, the market has wanted to own Johnson & Johnson (JNJ) despite subpar results. The large healthcare company trades near all-time highs just below $150 even after exiting a period where sales have failed to meet goals. My investment thesis remains bearish on the stock following another string of weak earnings.

Image Source: JNJ website

Raised Guidance To Nowhere

JNJ is a solid healthcare company with a minimal growth trajectory. The biggest issue is the stock valuation. The market always appears to come up with a reason to own the stock due to the company beating quarterly earnings targets and raising guidance while never really growing materially.

Q3 results were no different. JNJ beat EPS estimates by a solid $0.22 and the company smashed revenue targets by $927 million. The company has such a diversified revenue base in pharmaceuticals and medical devices that gains in one division typically are offset by losses in other areas. Even great revenue performers such as Darzalex and Stelara barely offset declines in other areas with these product sales only contributing ~5% and 10% of quarterly sales.

The issue is that JNJ only grew revenues by 1.7% after a linked quarter where sales slipped 10.8%. The company guided up for 2020 to a revenue target of $81.6 billion and an EPS goal of $8.00. Ultimately, the amount suggests Q4 results won't meet previous targets with the guide up only equivalent to a $0.15 hike from previous targets after a bigger beat in Q3.

The company entered the year with an EPS target above $9.03, so the raised guidance for the last quarter is still over $1 below original expectations for the year. Nobody can really blame JNJ for not maintaining targets due to COVID-19, but the problem here is the stock trading right near the all-time highs despite the far weaker results.

The stock actually trades at 18.5x these updated EPS estimates for 2020. Analysts now expect JNJ to return to the original 2020 EPS target of over $9 in 2021. Again, the company is generating solid results for the environment, but investors paying nearly 16.5x '21 EPS estimates is again rich for what the company actually delivers.

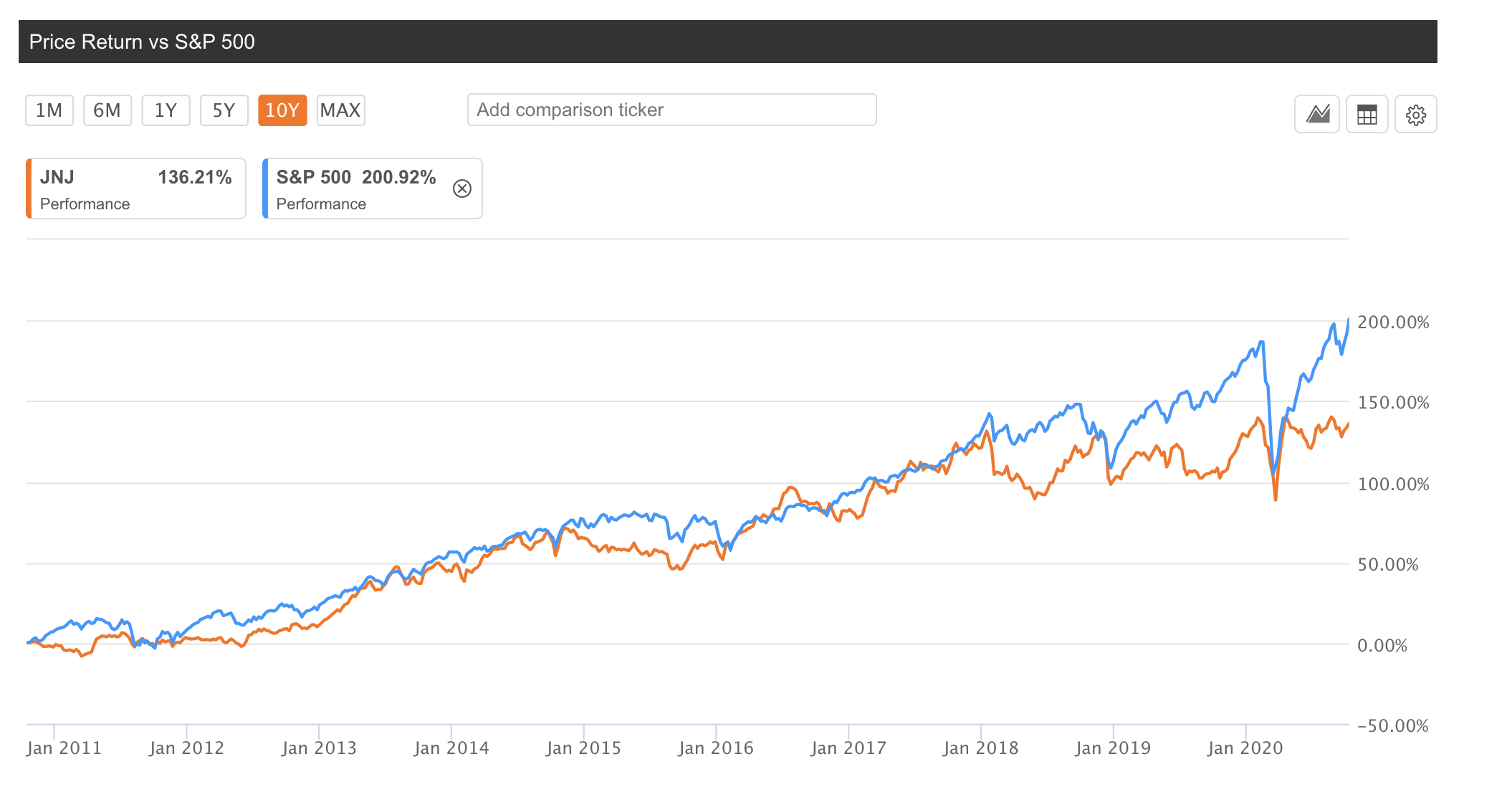

The price return versus the S&P 500 has struggled in the last few years when my warnings started for these very reasons. JNJ is priced for substantially faster growth leading to the reduced returns for investors piling into the stock and ignoring these common sense valuation metrics.

Source: Seeking Alpha Momentum