(Source: YCharts)

Summary

- Johnson & Johnson appears undervalued because its 16X P/E is below its historical norms.

- However, the business has evolved where an added presence from pharmaceuticals has brought increased risk to the company.

- We would like to see a small pullback to create a margin of safety in what remains a top-notch company and stock.

Healthcare conglomerate Johnson & Johnson (JNJ) has been a staple of dividend growth portfolios for decades. The company boasts an ongoing streak of 56 consecutive years of increasing its annual payout to shareholders. For nearly a quarter century, investors who have reinvested dividends have realized total annual returns of 11.5%, which can generate immense amounts of wealth over the long term. Today, Johnson & Johnson trades for nearly $140 per share, the upper end of its 52-week range. While this iconic name deserves consideration for any long-term stock portfolio, there are some things to consider before signing off on your purchase order at the current stock price.

The Stock Isn't As Cheap As It Appears

When you first look at Johnson & Johnson, the stock appears attractively priced, despite trading at the top of its 52-week range. Based on analyst-projected earnings for the full year of $8.59 per share, the stock's earnings multiple of 16.29X represents a 13% discount to its 10-year median P/E ratio of 18.7X.

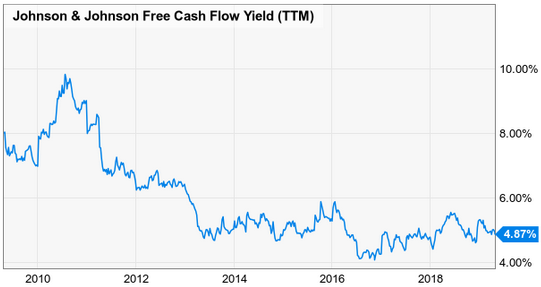

However, when we look at a few other valuation metrics, we get some conflicting results. When we look at valuation from a standpoint of free cash flow, the valuation has actually trended lower over the past decade. This makes sense, as the share price has been partially inflated by a strong bull market (rising tide lifting all boats type of effect). Despite Johnson & Johnson increasing its conversion rate of revenues to FCF over time (currently a robust 22%), the share price has outpaced this, pushing the yield lower.